Budgeting won’t fix poverty. Budgets are not magic wands that lead to stability.

But talking badly about budgets feels a bit icky. One, I’ve led community-based financial literacy programs, and two, we’re taught that budgets are the responsible thing to do. Three, I love numbers and spreadsheets.

Budgets absolutely have value. A budget helps people track expenses, prepare for minor emergencies, and organize their priorities.

But if you care about justice, about changing the conditions that keep entire communities stuck, personal budgets are only one tool among many.

They cannot, by themselves, address low wages, housing markets that squeeze renters, discriminatory or predatory lending, or a changing climate that makes basic needs more expensive.

Budgets can steady a household’s ship, but they can’t change the ocean. Our work, whether spiritual, political, or communal must address the systems that create the storms in the first place.

What budgeting can and can’t do

Budgets are a discipline. They make invisible trade offs visible.

Budgets can paint a vivid picture of how much of your monthly income goes towards rent or how one emergency room visit can send a family into debt.

For people with a stable, sufficient income, budgeting can help them save more money, plan for the future and reduce stress.

However, countless studies show that a large share of households lack basic emergency savings.

Systemic Drivers of Poverty that Make Budgeting Hard

Systems produce poverty.

Who sets the wages? Why are developers allowed to push out local homeowners? Who writes the policy that will enable corporations to skirt paying taxes?

These are policy and market choices, not personal failings.

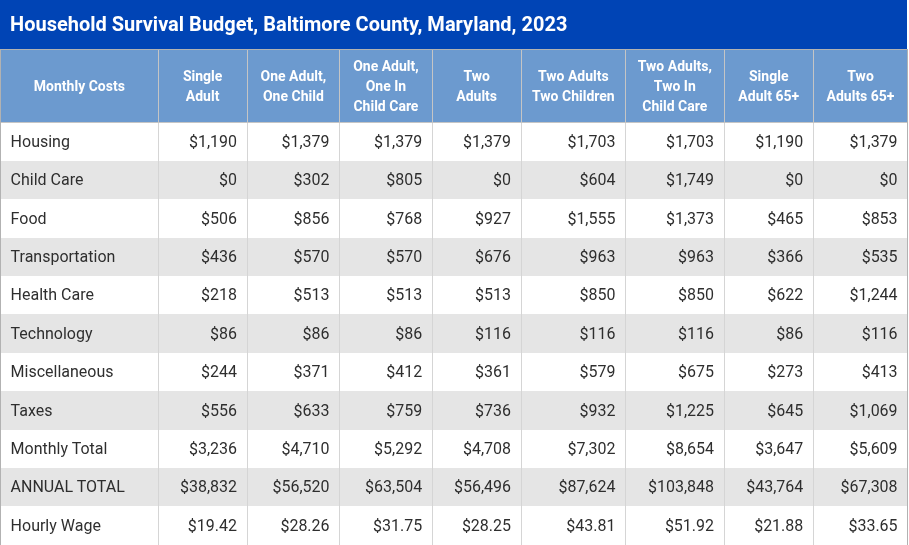

I worked briefly for the United Way as a Development and Marketing Manager. One amazing resource was an annual report the organization produced that calculated household survival budgets for families in each U.S. zip code.

The ALICE (Asset Limited Income Constrained Employed) report is the best indicator of financial strain families experience. For each zip code, a household survival budget is calculated. The budget reflects the minimum costs of household necessities (housing, child care, food, transportation, health care, and technology) plus taxes and is adjustable by household size.

ALICE families are employed, typically earn more than minimum wage, and are above the federal poverty level and ineligible for government safety net programs. However, their income is insufficient to meet the minimum day-to-day costs of living.

For example, in Baltimore County, Maryland, a family of four would need to make nearly $88,000 per year to afford basic expenses in 2023. That is more than double the Federal Poverty Level of $30,000 for a family of four.

That trend exists outside of Maryland. Throughout the United States, a working family needs well above the official poverty line to afford the basics.

ALICE may be your relative, friend, colleague, or neighbor, or you might be ALICE. ALICE may also be your health care provider, teacher, retail clerk, sanitation worker, and others.

That’s why telling someone to cut back or “be more disciplined” misses the target because for many people, there simply isn’t enough left to cut.

Click here to view ALICE data for your zip code.

What if the determinations for safety net programs used more realistic figures, like those from the ALICE data?

When “Good” Financial Advice Doesn’t Fit Real Life

Most financial advice often assumes stability that many working people simply do not have.

It assumes predictable income, accessible healthcare, safe neighborhoods, and time to comparison-shop. For many families, that’s not reality.

Here are a few examples of what we’re typically told and what is often true instead:

1. “Build a six-month emergency fund.”

If rent consumes half of your income and wages have not kept pace with costs, saving is difficult.

2. “Just get a better job.”

Anyone who says this isn’t looking at the latest job reports. This assumes mobility, access to training, childcare, transportation, and discrimination-free hiring. Labor markets are not neutral. They are shaped by race, geography, access to education, and immigration status.

3. “Cut out small luxuries.”

The daily coffee or avocado toast myths should be left to memes. Comparing those items to rent, healthcare premiums, and childcare is a distraction from the real questions, like why aren’t those things affordable?

4. “Invest early and consistently.”

True, but if you have disposable income. Also, certain investments may be difficult to liquidate quickly or may carry penalties or wait periods.

5. “Avoid debt at all costs.”

Sometimes debt is the only bridge available to cover medical bills, car repairs, or tuition. Debt can also be a form of financial leverage. The deeper issue is why necessities require high-interest borrowing in the first place.

What Actually Helps

If budgeting alone isn’t enough, what is?

Practical steps:

• Track spending, even if small, to create clarity.

• Build emergency savings where possible.

• Join community-based financial education programs.

• Participate in mutual aid networks.

Engage the Systems:

• Advocate for living wages and tenant protections.

• Support healthcare reform and fair lending policies.

• Engage in climate resilience and sustainable consumption initiatives.

• Enroll in banking services with public banks or credit unions

Discernment for Purpose and Justice:

• Ask how your skills intersect with systemic change.

• Explore communal action alongside personal stewardship.

• Align your financial practices with the values of solidarity, dignity, and collective well-being.

Budgeting is just the starting point. By combining practical stewardship with advocacy, mutual aid, and discernment for justice, individuals and communities can create meaningful financial and social transformation.

Subscribe to the Soulfully Rich Living newsletter for tools, frameworks, and strategies that help you navigate personal finances while engaging the systems shaping economic realities.

Soulful Takeaways:

• Budgeting helps individuals but not systems. Use budgets for personal decisions, but they can’t address systemic injustice.

• Poverty is produced. Wages, housing, credit, and policy shape it. Change those, and you change outcomes.

• Pair private practice with public action. Financial coaching + mutual aid + organizing for living wages is a stronger strategy than any of these alone.

• Find what you can do. Discernment helps connect personal resources and purpose to justice-oriented action.